How to Pick one of the most Trustworthy Secured Credit Card Singapore for Your Requirements

How to Pick one of the most Trustworthy Secured Credit Card Singapore for Your Requirements

Blog Article

Exploring Options: Can Former Bankrupts Secure Credit Scores Cards Adhering To Discharge?

Navigating the economic landscape post-bankruptcy can be a complicated task for individuals seeking to rebuild their credit report. One usual question that develops is whether previous bankrupts can efficiently obtain bank card after their discharge. The response to this inquiry involves a diverse expedition of various elements, from debt card options customized to this market to the influence of previous economic decisions on future creditworthiness. By understanding the complexities of this process, individuals can make enlightened choices that may lead the means for a much more safe and secure economic future.

Recognizing Bank Card Options

When considering credit cards post-bankruptcy, people must meticulously evaluate their requirements and economic circumstance to pick the most suitable choice. Guaranteed credit history cards, for circumstances, call for a cash down payment as security, making them a viable option for those looking to restore their credit scores background.

Additionally, individuals must pay close attention to the annual percentage rate (APR), grace duration, yearly charges, and rewards programs provided by various debt cards. By adequately examining these aspects, individuals can make informed decisions when choosing a credit report card that lines up with their financial objectives and scenarios.

Aspects Impacting Approval

When applying for bank card post-bankruptcy, comprehending the factors that influence approval is important for people seeking to reconstruct their financial standing. One critical aspect is the applicant's credit rating. Following a personal bankruptcy, credit history scores typically take a hit, making it more challenging to receive traditional bank card. Nonetheless, some companies supply protected credit scores cards that call for a deposit, which can be a much more attainable choice post-bankruptcy. An additional considerable factor is the applicant's revenue and employment condition. Lenders intend to ensure that individuals have a steady income to make prompt settlements. Additionally, the length of time given that the bankruptcy discharge contributes in authorization. The longer the period considering that the bankruptcy, the higher the possibilities of authorization. Showing responsible financial habits post-bankruptcy, such as paying costs on time and keeping credit rating usage low, can additionally favorably affect credit history card authorization. Understanding these elements and taking steps to enhance them can boost the chance of safeguarding a charge card post-bankruptcy.

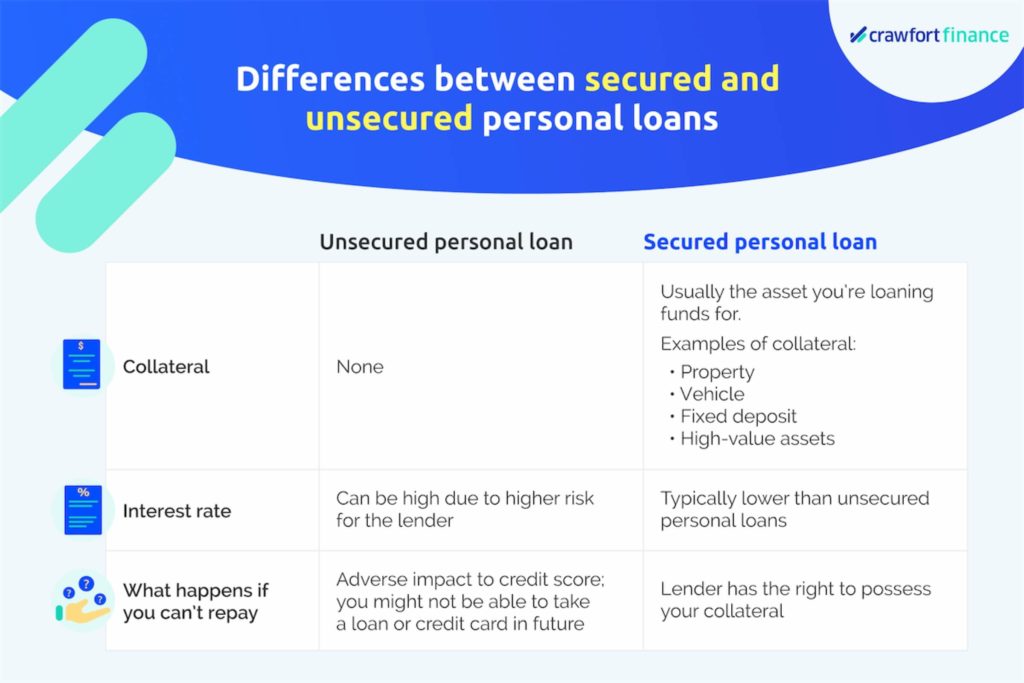

Secured Vs. Unsecured Cards

Comprehending the differences between unsafe and protected charge card is critical for people post-bankruptcy looking for to make educated choices on restoring their economic wellness. Safe charge card need a money deposit as security, generally equivalent to the credit score limitation prolonged by the issuer. This deposit minimizes the threat for the credit card firm, making it a feasible choice for those with a history of personal bankruptcy or bad credit scores. Protected cards frequently feature reduced credit line and greater rate of interest contrasted to unsafe cards. On the various other hand, unsecured credit rating cards do not call for a money down payment and are based exclusively on the cardholder's creditworthiness. These cards generally supply higher credit limitations and lower passion rates for people with good credit scores. Nonetheless, post-bankruptcy people might locate it challenging to receive unprotected cards promptly after discharge, making guaranteed cards a more viable choice to begin rebuilding credit. Eventually, the selection between protected and unsafe credit score cards depends upon the person's economic situation and credit score objectives.

Building Credit Score Responsibly

To effectively restore credit score post-bankruptcy, establishing a pattern of accountable credit report usage is important. Additionally, maintaining credit report card balances low loved one to the credit report limitation can positively influence credit score scores.

Another approach for developing credit rating sensibly is to keep an eye on credit scores records routinely. By reviewing debt reports for mistakes or signs of identification theft, people can address problems quickly and keep the precision of their credit rating. In addition, it is recommended to avoid opening several look these up brand-new accounts simultaneously, as this can indicate economic instability to possible loan providers. Rather, emphasis on slowly expanding credit history accounts and showing consistent, accountable credit habits with time. By complying with these practices, people can gradually restore their credit post-bankruptcy and work in the direction of a much healthier financial future.

Reaping Long-Term Advantages

Having actually developed a foundation of responsible credit rating management post-bankruptcy, people can now concentrate on leveraging their improved credit reliability for long-lasting monetary benefits. By continually making on-time repayments, keeping credit rating application reduced, and monitoring their credit rating records for accuracy, previous bankrupts can slowly reconstruct their credit rating ratings. As their credit rating raise, they may become qualified for better debt card uses with reduced interest prices and higher debt limitations.

Gaining long-lasting gain from improved credit reliability extends past simply bank card. It opens up doors to favorable terms on loans, home loans, and insurance policy premiums. With a strong credit rating, individuals can work out far better rates of interest on finances, potentially saving hundreds of dollars in interest settlements with time. Additionally, a favorable credit scores account can enhance job leads, as some companies might check debt records as component of the working with process.

Conclusion

To conclude, previous insolvent individuals may have problem protecting bank card complying with discharge, however there are alternatives available to help rebuild debt. Understanding the different types of bank card, variables impacting approval, and the significance of accountable bank card use can aid people in this scenario. By picking the best card and using it properly, former bankrupts can slowly enhance their credit report and enjoy the long-lasting benefits of having access to credit history.

Demonstrating responsible financial actions post-bankruptcy, such as paying costs on time pop over to this web-site and maintaining credit score application reduced, can likewise positively influence credit card authorization. In addition, maintaining credit history card balances low loved one to the credit scores limitation can positively influence credit score scores. By regularly making on-time settlements, maintaining credit report usage reduced, and checking their credit history reports for precision, former bankrupts can gradually restore their credit score scores. As their credit ratings enhance, they might end up being Homepage qualified for much better credit rating card supplies with lower passion rates and higher credit rating restrictions.

Understanding the various types of credit score cards, elements influencing approval, and the value of responsible debt card usage can assist people in this situation. secured credit card singapore.

Report this page